The Story Phase: The Urge to Own Stuff Today

In 1923, Henry Ford found himself with quite the dilemma.

Fifteen years earlier, the Model T had completely reshaped the automobile industry. A machine once reserved mostly for the wealthy was now within reach of an ordinary American family. By making cars simpler and manufacturing them at an enormous scale, Ford was able to push down the price of ownership.

Well… almost.

Even after Ford had reduced the price considerably, a car was still a major purchase. For many working families, it was still too expensive to buy in one go.

General Motors, one of Ford’s largest competitors, had found a solution for this.

A few years earlier, in 1919, they created the “General Motors Acceptance Corporation,” better known as GMAC. Instead of asking customers to pay the full price upfront, GMAC allowed them to make a down payment, take the car home, and pay the remainder over time.

To us, this does not sound particularly radical at all. Because, in the United States alone, 83 percent of new-car buyers financed their purchase in the first quarter of 2026.

And compared with today’s financing, GMAC’s early loans were still quite conservative. Many required roughly 35 percent upfront, with the rest paid within a year. Today, some car loans stretch beyond six or even seven years.

But underneath the economics, this was a huge psychological leap.

With this new down payment plan, the car buyer does not need to answer the question: Do I have enough money to buy this car?

Instead, the question they have to ask is more simple, and quite less worrisome: Can I manage the monthly payment?

Henry Ford did not like this approach. He believed people should save before buying something.

So, in 1923, Ford introduced the Weekly Purchase Plan.

A customer could deposit a few dollars each week with a Ford dealer. Once the deposits added up to the full price of the car, they could finally take it home.

But you and I already know who won this financing battle.

GMAC’s monthly payment plan spread so quickly, and it’s quite easy to see why. There was no need to spend years planning and saving before you finally get your hands on the shiny new car. You could walk into a dealership, make the first payment, and drive it home that day.

So, Ford’s savings plan struggled, while instalment buying became increasingly common. In 1928, Ford finally established its own vehicle-financing company. By 1930, more than two-thirds of American automobiles were being bought through instalment payments.

Everybody wanted stuff today, right now.

But there was a huge compromise hidden inside this newfound convenience.

A car bought this way is more than a car. It is also a promise made to the future self.

Or, put another way, it is a bet placed on our future self: that we will continue earning enough, remain healthy enough, and have enough potential to keep paying for the stuff we bought.

The Structure Phase: The Pressure Is Being Forwarded

Seen this way, Ford and General Motors were not only offering two different ways to buy a car. They were offering two different ways to distribute the stress that comes with a large purchase.

If you buy the car with cash, the pressure remains with you in the present.

Under GM’s financing model, though, the pressure moves into the future. You receive the car immediately, but automatically commit a substantial part of your future income to paying for it.

And many Western economies have gradually built themselves around this credit culture, where homes, cars, phones, and even furniture can be brought into the present through monthly payments.

For example, by the fourth quarter of 2025, Canadian households held about $1.79 in credit-market debt for every dollar of disposable income. Canada also had one of the highest household debt-to-income ratios among wealthy countries.

Is this all bad?

Of course not.

This credit system can be a powerful tool for building wealth or expanding access for building wealth.

- A mortgage, for example, lets someone buy a home before they have saved the full price and slowly build equity over time.

- Student loans can give someone access to an education they otherwise could not afford, which is also an investment to build more wealth later in life.

- A business loan can help someone buy equipment, hire employees, or expand a business before they have accumulated all the money required to do so.

But the downside of this system is rarely talked about.

Why?

Because it’s a little like a fast-food chain trying to promote intermittent fasting. There is no business model in asking people to consume less.

But sometimes, eating less is good for us.

The same applies to credit purchases.

When we buy something with cash, the pleasure attached to whatever we are buying and the burden of paying for it are fused together.

There is a psychological coupling between consumption and payment.

This creates necessary economical friction. It forces us to stop and think about whether the purchase we are about to make is really worth it.

Imagine seeing a $1,200 espresso machine in an Instagram morning-routine video. It looks promising.

But when you have to pay $1,200 in one go, you’d probably think harder whether you really need it.

But, presented as $50 a month, it’s not that much a big deal:

Can I afford another $50 payment?

And now, it’s just “set it and forget it” type deal. And now you don’t even think about what else that $50 could buy in the future. The decision is too quick for you to even realize what you’re giving up.

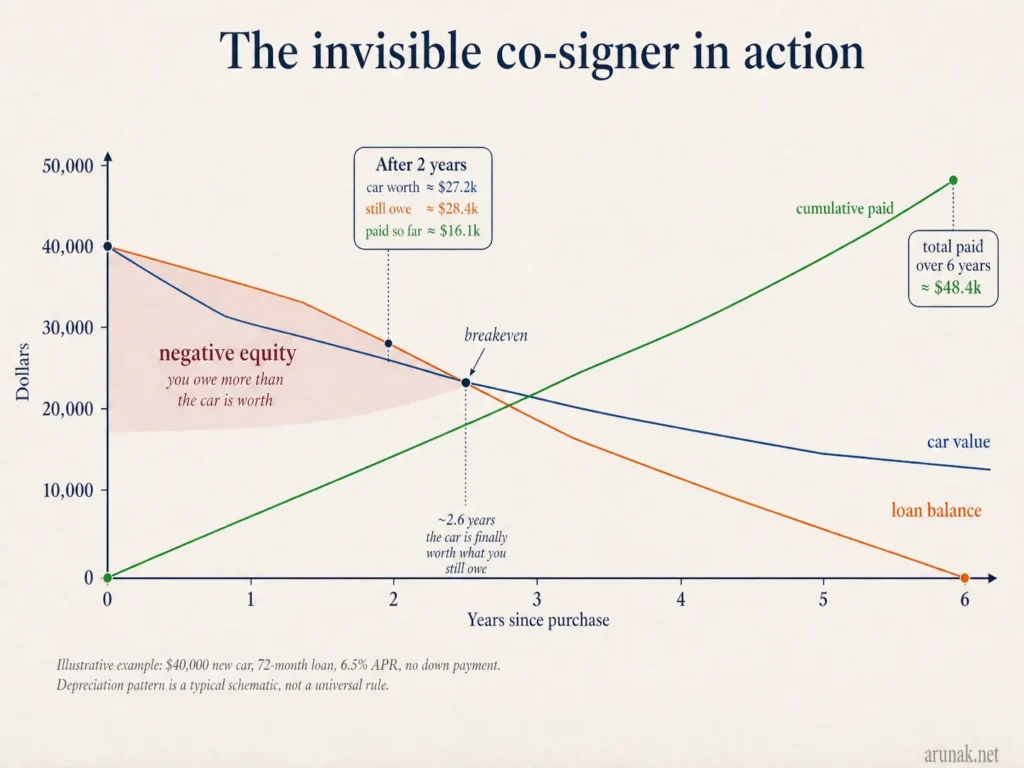

In other words, we forget that our own future self is the invisible co-signer on every monthly payment.

Like this, we place that future self under a kind of pressure that neither of us could fully predict when the agreement was made.

The Interface: The Agreement with Both the Selves

But again, this is not to say that the monthly payment model is inherently bad. It is, however, quite important to have both our current self and future self agree on the purchase, which is often not the case.

- A useful place to start is by bringing the full amount back to the table before making a purchase. Do not ask only, Can I afford $650 a month? Ask how much the car will cost after interest, insurance, maintenance, fuel, and the loss in value.

- Then test the payment against a “bad month,” not an ordinary one. Could you still pay it comfortably if things went sideways?

- And then think about the opportunity cost. How many months of work are you committing to this purchase? How much of your future income is already spoken for because of it? What else in your life becomes a sacrifice in order to keep it?

The goal, though, is not to make every decision perfectly safe. It’s impossible. There is always a certain amount of risk attached to any decision you make in life, even if you consider yourself a very risk-averse person.

But by doing this, we make sure that the choices we may need to make in the future, in order to become the person we aspire to be, are not being quietly restricted by the person we are today.